Call For Consultation

Call For Consultation

WILL HOMEOWNERS BE AFFECTED BY THE NEW FEDERAL TAX LAW?

- posted: Jan. 18, 2018

- Real Estate

Updated March 27, 2018 Congress recently passed and President Trump signed into law a sweeping overhaul of the federal income tax structure. The experts are still sorting out all of the various parts of the very complicated law and its potential impact on individuals and businesses. Discussed here are some of the changes in the tax code most likely to affect residential homeowners. This blog presents a broad overview, so it is important that each individual consider their own tax situation and discuss any questions regarding their taxes with a tax professional.

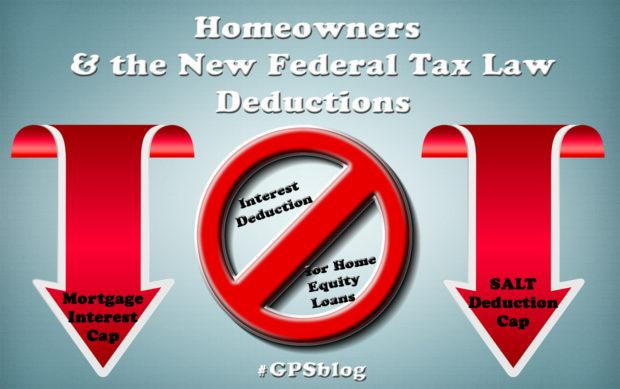

There are three specific provisions that may directly affect residential homeowners.

Cap on Amount of Mortgage Interest Deduction: Under the new law, the maximum loan amount on which interest may be deducted is decreased to $750,000 from the current $1,000,000. This means that only interest paid on the first $750,000 in mortgage debt is deductible. Note that this change only affects new mortgage originations; it does not change the limit for mortgages already in place. The law also continues to allow interest on mortgages for first and second homes to be deducted.

Deductibility of interest paid on home equity loans: When the new tax law was first passed, it appeared to eliminate the deduction for interest paid on home equity loans. Under the prior law, interest paid on home equity loans up to $100,000 was deductible. Based on recent guidance from the Internal Revenue Service, the deduction for home equity loan interest (as well as interest on second mortgages or home equity lines of credit) will continue, as long as the proceeds of the loan are used to buy, build or substantially improve the taxpayer’s home. If the proceeds are used for other purposes, such as to pay off credit card debt, the interest paid would not be deductible. The amount of the home equity loan will be counted towards the cap discussed above. For the IRS guidance, click here ( https://www.irs.gov/newsroom/interest-on-home-equity-loans-often-still-deductible-under-new-law)

Cap on state and local tax deduction: The change most likely to be felt by homeowners in Connecticut is the new cap of $10,000 on the deduction of state and local taxes (“SALT”). Currently any amount paid on SALT (state income tax and local taxes paid on cars and homes) is deductible for most taxpayers. The final tax legislation capped that amount for all taxpayers at $10,000 total. For many Connecticut homeowners, between their car and house taxes, they pay over $10,000 without even taking into account their state income tax payments. This is the change likely to have the greatest impact, especially in towns with high property taxes.

Keep in mind that this blog post just describes three provisions out of many that are in the new tax law, which also decreases rates and increases the standard deduction. However there is no doubt that the new law affects some of the deductions that homeowners have taken for granted.

- Business & Contracts (28)

- Covid19 (16)

- Criminal & Traffic Defense (27)

- Elder Law (26)

- Finance (3)

- Firm News (5)

- Foreclosures (2)

- Injury & Accidents (57)

- Insurance Law (17)

- Labor & Employment (61)

- Product Liability (1)

- Personal Injury (59)

- Family Law (1)

- Bankruptcy (1)

- Auto Injury (12)

- Estate Planning (10)

- Workers Rights (1)

- Business Law (2)

- Wills and Probate (1)

- Truck Accidents (3)

- Divorce (1)

- Employment (1)

- Auto Accident (2)

- Pedestrian accidents (1)

- Dog bites (1)

- Bicycle Accidents (1)

- Nursing Home (1)

- Catastrophic Injury (1)

- Legislative (1)

- Wrongful Death (1)

- Auto accident (1)

- Landlord & Tenant (6)

- Litigation (38)

- Medical Malpractice (5)

- Municipal Law (3)

- Real Estate (48)

- Supreme Court Rulings (5)

- Trusts, Estates, Wills & Probate (34)

- Workers' Compensation (12)

- Zoning, Planning & Land Use (3)

Contact Us

Please tell us about your legal matter and a member of our staff will contact you.

Map & Directions

Gesmonde, Pietrosimone & Sgrignari, L.L.C. is located in Hamden, CT and serves clients in and around North Haven, Hamden, Waterbury, Bethany, Milford, Wallingford, Prospect, Woodbridge, Northford, Madison, Beacon Falls, Branford, Cheshire, North Branford, East Haven, Naugatuck, Meriden, Ansonia and New Haven County.

Attorney Advertising. This website is designed for general information only. The information presented at this site should not be construed to be formal legal advice nor the formation of a lawyer/client relationship. [ Site Map ]

See our profiles at Lawyers.com and Martindale.com

Martindale-Hubbell and martindale.com are registered trademarks; AV, BV, AV Preeminent and BV Distinguished are registered certification marks; Lawyers.com and the Martindale-Hubbell Peer Review Rated Icon are service marks; and Martindale-Hubbell Peer Review Ratings are trademarks of MH Sub I, LLC, used under license. Other products and services may be trademarks or registered trademarks of their respective companies. Copyright © 2024 MH Sub I, LLC. All rights reserved.